Profitable USA invoicing and payment collection, for Canadian entrepreneurs

Introduction

With a potential market next door that’s over 10 times the size of the domestic customer base, most Canadian entrepreneurs are interested in the American market. With a free trade agreement in place, and our familiarity with visiting the country, one might assume that invoicing and collecting payments is trivial. With a bit of planning however, you can make your customers in the USA happier, get paid much faster, improve how you work with suppliers, and avoid a big chunk of your export profits being diverted to your bank. While there are many other articles on most of the subtopics and service providers covered here, I hope you’ll find this more holistic approach helpful in making the right decisions for your business. The recommendations presented in this article are suitable for individual freelancers and small e-commerce ventures but apply to larger, established companies as well. This article is written from a Canadian perspective but the recommended solutions are not specific to that country, as it turns out. I’d like to help others avoid the mistakes I made running a software startup while moving between Vancouver, New York City and North Carolina, and back to Canada (like unnecessarily setting up a US subsidiary!). For professional advice, I suggest consulting an accountant with both US and Canadian professional designations. I have included some affiliate links but that has not influenced the content of this article.

The Problem

What is the cost of not optimizing your international transactions? Imagine you collect funds from US customers, and that you also have US suppliers that expect US funds as payment (consider all your spending on online advertising and web applications, Amazon, imported equipment, etc.). If a customer wires you US dollars (USD), TD Bank may give you (assuming a 1.255 mid-market rate) Canadian (CAD) $1.22 for each dollar, less wire fees. Then you pay US suppliers with your TD Canada credit card, where each US dollar will cost you CAD$1.29. In that example, 7% of your gross revenue could be lost to currency conversion spreads. (If an average corporation’s net profit margin is around 10%, a few percent here and there can really reduce the value of making a sale.) There’s no need to operate that way, but your bank’s suggestions to optimize this are not going to be very helpful. You can set up a Canada-based USD account, but now cheques may take a month in the mail and another month to clear, and what can you do with those greenbacks from that account? (The short answer: Not much!)

Just use PayPal, you say? PayPal is one of the simplest solutions for some small businesses. You can accept credit card payments in USD (they charge a premium for USD payments: 2.9% + 0.8% + $0.30), and then use that money to pay US suppliers, thus avoiding the double conversion issue. However, when you want to get your money out, you’ll find that you cannot link your Canadian PayPal account to a USD bank account, and instead you have to use PayPal to convert to CAD. At that point, PayPal will take an additional 4.0+%. Of course, your US suppliers may not accept PayPal, you might deal with larger dollar values or want to avoid the risk of PayPal locking your account (a topic discussed extensively in other blogs), or you might want to make payments to suppliers by cheque or ACH (explained later), so PayPal may not meet your needs.

The costs and issues with using the obvious choices of a Canadian USD account and credit card, and PayPal Canada are illustrated in the following diagram. Of course, fees and rates are subject to change, but this article will help you eliminate most of them!

The Solution

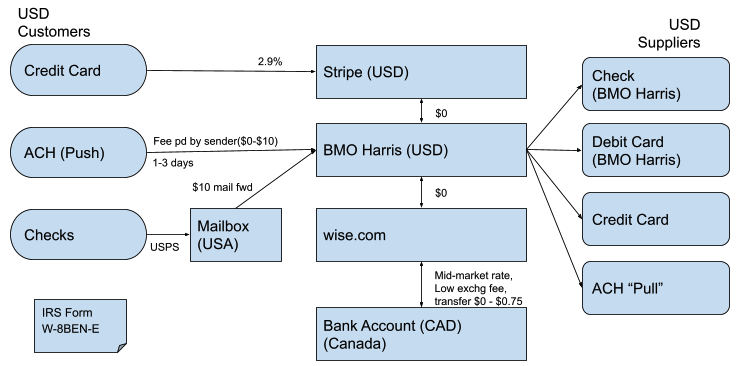

We’ll discuss American customers, currency exchange, cross-border banking, receiving and making electronic and cheque payments, multi-currency invoicing, and the Internal Revenue Service (IRS). You may end up choosing a solution that looks more like the following diagram, all aspects of which we’ll discuss in detail:

Understand Your Customer

How will this article help you make your customers happier? First of all, they’ll appreciate having more payment options, such as ACH. Secondly, you can just about eliminate the complications of asking them to deal with a foreign country. Canadians are so used to dealing with the US that they may not be aware of how little Americans deal with Canada. Consider the hassle of dealing with a foreign country, for possibly the first time. Canadians are used to buying “U.S. stamps”, i.e. postage for U.S. destinations, but there is no corresponding concept of “Canadian stamps” for the other direction. No American walks into a drug store and asks the cashier for Canadian postage; rather, they may have to take a trip to a busy, slow, fortified US Post Office and purchase international stamps just so they can mail you, their Canadian vendor, a cheque. (They are likely used to sending paper cheques to their domestic vendors using a quick online service provided in their online banking - a concept that does not exist in Canada and that doesn’t work for international payments.) The US Dollar is (for now, at least!) the preferred currency for international commerce, and accepting it may be a prerequisite for doing business in the USA.

Currency Exchange

This article started out with a discussion of the high fees charged by Canadian banks for currency exchange. Ultimately, you may want to use your greenbacks to pay yourself and your team nicely in CAD salary and dividends.

UK-based wise.com (formerly TransferWise) is disrupting the currency exchange business. By locating in many different countries, they take a very different approach and perhaps don’t actually need to move money when you do an international transfer. As a result, their fees are dramatically lower, allowing you to easily move money between your banks, to suppliers, and from your customers, by (cheap!) wire transfer, ACH, EFT, etc. You will never want to deal with a bank again after seeing how easy and inexpensive these transactions are using wise.com. Your wise.com account can be used for both personal and corporate use, with the two being kept separate. wise.com has made both my business and personal international transactions quick, inexpensive, and painless, although they can be a little optimistic in their estimation of transfer time. They ask for a minimum of information to get started, but expect more questions and required documentation as your dollar volume and needs increase. You can get started with a free transfer credit using this link.

Update 2023 The new Canadian fintech company tryvault.com is just like Wise but limited to Canadian corporations, claiming to offer better rates (I haven’t checked that claim), and adding a GIC feature. As with Wise, there is no way to accept cheques.

wise.com will work with any banks you choose. Curiously, if you want to convert from CAD to USD, TransferWise is listed as a bill payment payee at BMO and Manulife, but not TD Canada or RBC. Bill payments are not your only option.

As mentioned later in this article, wise.com can also function like a limited US business bank account. wise.com does have competitors like XE.com and KnightsbridgeFX which I have not reviewed.

If you’d like great customer service from a Canadian service provider, another excellent alternative to banks is Vancouver-based VBCE Online, a service of Vancouver Currency and Bullion Exchange - a real brick-and-mortar business. You’ll provide them with the details of your CAD and USD bank accounts, whether each is in Canada or the US, and they’ll provide you with a simple web interface for booking transfers between your account with an excellent exchange rate. Accounts go through within a couple days and there are no transaction or monthly fees. VBCE works for everything from getting cash for your vacation, to transferring funds to a US subsidiary corporation. My guesstimate is that they cost 0.65% more than wise.com, but that could depend on who you are and how much you are converting, and unlike wise.com there are no additional wire/EFT/ACH fees.

Cross-Border Banking

Most major Canadian banks offer a USD account for Canadian business customers. As with anything, just because someone offers it doesn’t mean that it is a good idea! Yes, most likely they’ll accept cheques drawn on a US bank. They may, however, do so very reluctantly. You’ll want to allow a month for cheques to clear. An RBC Express representative told me that in some cases (presumably larger amounts), banks will insist on converting a cheque to a wire transfer, and of course in that case the fees will be deducted. This processing delay is of course on top of any time spent in the mail (typically almost 30 days via the United States Postal Service (USPS) from New York to Vancouver during the 2020/21 pandemic).

OK, so your cheque deposit cleared? Great! Now what? Withdraw it as cash? You can’t make electronic payments to the USA. Your US suppliers may not accept a cheque drawn on a non-US bank. You can convert it to CAD, giving 3.5% of your sale to your bank, or get a much better rate using one of the online currency exchange services we discuss in this article. US and Canadian banking uses some of the same terminology, so it can be confusing and you may think you can do something that you cannot. Canadian electronic funds transfers (ETF) are not compatible with the US Automated Clearing House (ACH) system for electronic payments. A US routing number and a Canadian routing number are different things. The bottom line is that you can’t do anything in the USA with your Canadian USD account. We will discuss some alternatives that may be better than opening a USD account at a bank located in Canada.

If you are only going to accept electronic payments from customers (no cheques), you may be able to get by with wise.com (formerly TransferWise). wise.com will let you quickly and easily set up a “virtual” US bank account for your business, with appropriate routing and account numbers for a one-time fee of around $50. I don’t recommend this because of its limitations due to not being a real bank account, such as no deposit guarantee, no micro-deposit account verification for ACH, and no debit card. (Skip the $50 fee and use a free wise.com account for cheap currency exchange and wire transfers as explained elsewhere in this article.)

Canadian banks know that doing business in the USA is important, and at first glance it looks like they are here to help! (Spoiler alert: they’re not that helpful yet, but they’re working hard at it.) Canadian banks are big players in the highly fragmented and regional US banking industry. TD Canada Trust’s “TD Bank N.A.” is the 9th largest bank in the USA, after acquiring Banknorth and Commercebank (https://en.wikipedia.org/wiki/TD_Bank,_N.A.), serving 15 East Coast states. The Royal Bank of Canada owns RBC Bank (Georgia). BMO Bank of Montreal acquired Harris Bank, now BMO Harris, based in Chicago. CIBC (aka the Canadian Imperial Bank of Commerce) owns CIBC Bank USA (formerly PrivateBancorp) in the Midwest. Desjardins and National Bank (NatBank) have banks in Florida. And of course, HSBC is popular with Canadian businesses and is a leader in global banking including the USA ($1.9 billion in IRS fines for international money laundering in 2020 attest to that!). Scotiabank is a global bank but surprisingly does not have retail operations in the USA.

Some of these Canadian banks will happily tell you about their cross-border banking services for individuals, but you’ll want to get to a major downtown branch or the right department in a call centre to get accurate information about their business services (my suburban RBC branch manager knew nothing about this but he tried really hard). What your Canadian bank won’t tell you is that you’re far better off going directly to the US subsidiary and bypassing your fellow Canadians! To get cross-border banking services from RBC Canada, for example, you first need to go through the long process of opening a bank account (I spent an hour at a teller in-person during the worst of the pandemic to activate a business debit card I had no interest in using) and then sign up for a murky, mysterious, customized offering called RBC Express. One part of RBC Express is the ability to pay US suppliers electronically - i.e. a real US-based account, the holy grail! How much does it cost? I wasn’t able to get a clear answer to that question. There may be an ACH setup fee. There may be monthly fees. There may be transaction fees. Maybe it costs more if you need more than one employee to have access. I spent hours on the phone with my branch and with an RBC Express representative, and I still don’t know. I expect that it is not worth the trouble or expense at this time. I closed our RBC account shortly after opening it.

Let’s cut to the chase (no, not Chase Bank). I went with the Essential Business Checking Account with BMO Harris. It provided everything I needed, essentially for free: Their $12 monthly fee is waived for a minimum average balance of $1,500. Sure, the account opening process is substantial, but the representative I dealt with was exceptionally knowledgable and claimed they do this for Canadian businesses every day. After my RBC Express experience, and after dealing with TD’s newly acquired US branches in Manhattan where the staff hadn’t yet learned about their new parent company’s cross-border banking services, it was refreshing to deal with a banker (just one - a representative is assigned to support you throughout the account opening process and you won’t spend time on hold) who knew exactly what he was doing. Yes, they need a lot of documentation, but with the IRS keeping a close watch on everything that is understandable. And there are no surprises; BMO Harris tells you exactly what you’ll need to do and warns you that the process will take up to a month to complete. Once your account is open, you’ll be all set to transact with your southern customers and suppliers. Unfortunately, you can’t start with an online application, but instead you have to phone them and explain that your business is in Canada.

Have I tried opening a Canadian-owned business account with any other US banks? No. Could another bank be just as good? Yes. Could it be better or cheaper? Probably not. I had only one glitch with the BMO Harris account opening process, and that was due to ignoring a clear instruction. However, since all US banks are regional (unlike in Canada, no bank has a branch in every state), if you like the old-school idea of being able to visit a branch you may want to consider which bank has branches in a state you regularly visit.

Receiving Payments by Cheque

The governments of the US and Canada may not agree on the spelling of cheque / check, the routing number scheme is different, and Americans may be able to send a cheque just by submitting a form in their web banking, but otherwise, cheques work basically the same way in each country. But now that you’ve opened a bank account in Chicago for your Canadian business, how are your customers’ payments going to be deposited? Easy. Use the mobile deposit feature of the bank’s mobile app, or bank by mail. BMO Harris has very efficient banking by mail that works with either the postal service or couriers, and they immediately mail you a deposit record via Canada Post (not USPS!). I’ve seen payment show up in my bank account 2 days after my customer put the cheque in the mail - faster than regular ACH electronic payment!

As mentioned earlier, your customers may not be used to dealing with international postage, and you may not want to wait a month for the cheque in the mail. To avoid these issues, if you don’t have an agent of some kind to do this for you, you can sign up for a US mailbox service that includes mail forwarding. Even better, your mailbox service may be able to prepare your cheques for deposit and send them straight to the bank, avoiding cross-border mail delays. If you receive payments from a close business associate such as a reseller, you could potentially have them send cheques directly to the bank in the same way. I ordered custom-made deposit stamps from VistaPrint for $6 each (sale price) to eliminate worries about third parties making mistakes in the endorsement and to ensure the correct bank account number is used.

There are two main kinds of mailbox services to choose from: a private mailbox franchise location (e.g. UPS Store, PostNet, etc.), or an online virtual mailbox and scanning service. These are not as different as they sound; the latter are software companies that are layered on the former (your mail is delivered to a virtual box number at a UPS Store, for example, and then is forwarded to the mail scanning service). Besides handling cheques, these services can handle any mail you want to receive at a US address, and may be able to forward parcels to Canada. While a mail scanning service will have a clear price list for things such as cheque forwarding, the UPS Store refers you to each location for any questions with regard to mail forwarding and other services. At the UPS Store, your friendly store owner may be happy to email you when mail arrives, or endorse and forward cheques to your US bank and just charge you for the postage. It’ll be an informal arrangement, and if she forgets to endorse the cheque before mailing it, well, the bank will probably be OK with that.

If you’d like to take a more formal, technologically-advanced approach, there are a number of virtual mailbox options, including:

- EarthClassMail

- Traveling Mailbox

- PhysicalAddress.com

- ipostal1.com

- AnytimeMailbox.com

EarthClassMail may be the most business-oriented choice, with the ability to connect to Dropbox and Google Drive, and even to your accounting system for check deposits! I have used Traveling Mailbox addresses in New York City (a UPS Store) and in their home state of North Carolina (PostNet). You can have 3 business and personal names associated with your mailbox, which costs $15 - $20 per month or more depending on your volume of mail. They’ll scan your incoming mail and notify you electronically, and they have a great web application for viewing your mail and choosing whether to shred or forward each item. Cheques can be automatically forwarded to your bank for a $4.95 service charge plus USPS postage ($5.95 with proof of delivery). Mail forwarding is $2 plus postage or courier fee per shipment.

Some virtual office services (e.g. Regus, in bankruptcy at time of writing) and coworking businesses also offer virtual mailing addresses, but those seem to be unlikely to offer cheque forwarding. Stripe’s cheque handling is not available to Canadian companies. Credit card processor Stripe, discussed next, accepts cheque payments directly via a P.O. box - but not for Canadian companies unfortunately.

Receiving Electronic Payments

Credit cards and wire transfers work just the same on both sides of the border, but other electronic payments methods are different.

If your customers pay you by wire transfer, and they use a bank rather than wise.com, it will typically cost ~$45 on the sending end and ~$25 on the receiving end, but where it really makes money for the bank is in the currency exchange rate. And avoiding exchanging currency is not always possible. When I recently tried wiring USD to Canada without currency conversion, Bank of America refused to do it, saying that they were required by law to disclose all fees, and they didn’t know how much the intermediary bank(s) would charge (according to my receiving bank (TD), Bank of America WAS the intermediary bank).

If credit card and/or debit card payments are suitable for your business, your Canadian bank may steer you to Moneris, the dominant Canadian credit card processor founded by RBC and BMO. Naturally they will accept multiple currencies, but predictably they’ll only settle with you in CAD. As mentioned earlier, PayPal Canada also does not allow you to withdraw USD (you’ll have no way around their poor exchange rate) and their credit card processing fees will add up to 3.7%. A very popular newer alternative is Square, with perhaps the best rate, charging only 2.65%. Stripe Payments is close behind, with fees of 2.9% + $0.30, and I’m going to rave about them later in this article when we discuss multi-currency invoicing. Unlike PayPal, Stripe lets you transfer funds directly to a USD bank account in Canada or to your wise.com account. A single Stripe login can be associated with independent CAD and USD accounts, so you can accept each currency and transfer receipts to separate bank accounts.

In Canada, your customers may pay you electronically using direct deposit or Interac e-Transfer. In America, it’s all about ACH. Automated Clearing House (ACH) comes in “push” and “pull” flavours. “Push” is when your customer signs in to their online banking and sends you the money; they just need to know your routing and account number. “Pull” is when you yank the money right out of their account. Yikes! In practice, a customer would click the payment link on your invoice, and choose to pay using their bank account details instead of a credit card. QuickBooks Payments or plaid.com make this easy for American companies. Unfortunately, you’re not going to get to “pull” if your company is not based in the USA.

Back to “push” then. If you’ve set up a US-based bank account or wise.com, ACH is easy. Make a note of your BMO Harris account and routing numbers (or, after paying the $50 fee, get your wise.com account and routing numbers as explained earlier), and happily give that information to your customers if they ask. (Unlike in Canada, there is no third number to identify the bank.) There is no fee to receive ACH payments, but there may be a fee to send them. Your customer can choose 3 day ($0-$3) or next-day transfers ($7-$10). However, not all banks provide this capability to their business customers.

Multi-Currency Invoicing

If you’ve read this far, you’re going to want to invoice your American customers in USD. Does your invoicing software allow you to invoice in USD as well as CAD? It might not! For example, with the Canadian accounting software Wave (www.waveapps.com), you cannot invoice in two currencies from one business, according to this great article for Canadian freelancers . Maybe you can just customize your invoices in a word processor, but this could be problematic if you automatically send your invoices and collect payments electronically. Choosing an invoicing solution, or addressing a shortcoming of an existing one, is beyond the scope of this article. To illustrate the issues, I will explain why I chose Stripe even though I was already using QuickBooks Online for Canadian invoices and PayPal for Canadian credit card payment acceptance.

Quickbooks Online (QBO) allows you to configure your company for multi-currency, and can invoice each customer in the correct currency. However, you can configure only one address to show on your invoice (i.e. no US address for US customers). If you want your invoice to include a prominent electronic payment link, only Quickbooks Payments is supported, although you could put your own link somewhere (my customers NEVER noticed a payment link in the footer!). Quickbooks Payments (Canada) converts USD payments to CAD at a disadvantageous rate, with no option for linking a separate USD bank account for those payments.

PayPal has excellent basic invoicing capabilities for businesses, but the shortcomings for USD revenue were discussed in the first part of this article. Many times customers have called us, asking to pay over the phone by credit card (because they didn’t see the payment link on their QuickBooks invoice) and we’ve had to say sorry, we can’t enter your credit card manually. PayPal likes to encourage people to sign up as PayPal users, so their basic account doesn’t give you the option to enter a customer’s credit card information manually. You can however sign up for Virtual Terminal ($35/month) to add that capability.

On the other hand, Stripe Invoicing gives you total control, is suitable for any size of business, has a well-documented API, and can integrate with many accounting systems. The cost depends on what parts of Stripe you use: Stripe Payments (credit/debit card acceptance costs discussed earlier), Stripe Invoicing, and if you want them to take care of recurring invoices, Stripe Billing. Invoicing Starter includes 25 free invoices per month; after that you’ll pay 0.4% per paid invoice. Keep in mind that this charge only applies to payments made via Stripe; if payment is made outside of Stripe (e.g. via cheque) then you can manually mark invoices as paid, and there is no charge.

Although they are very software developer-friendly, they have a ready-to-use manual Stripe Dashboard that supports invoicing and payment collection in many different currencies, including entering their credit card information manually. Your Stripe login can connect you to independent CAD and USD accounts, each with their own customer list, invoices, mailing address, and bank account connection, thus avoiding unnecessary currency conversion. At the moment, the provided invoice design is not very customizable, but that is evolving over time. For more customization, you can create invoices elsewhere and use Stripe to accept payment. Your web designer can add a Stripe Customer Portal to your website to provide your customers with access to invoices and payment. And as your business grows, Stripe really has no limits in terms of its ability to integrate with other software systems.

We’d all like to have our invoicing set up correctly the first time, and have it handle all of our US and Canadian customers. It’s just not as easy as it sounds, and you may want to have a software developer help you streamline your billing and payment processing system.

We’ve published a simple but complete example of a web application for accepting invoice payments via Stripe:

Paying Suppliers

You can of course write cheques on your US bank account. Your suppliers will appreciate (or insist on!) not receiving a cheque drawn on a foreign bank.

BMO Harris does not enable ACH payments (“Push”) in their online banking for customers who do not have a US address. However, you can use ACH “Pull” (explained earlier) to make payments to many suppliers who accept payments through their website.

wise.com gives you several options including the ability to send domestic wires to your suppliers inexpensively. (You can use wise.com for same-currency transfers, not just currency exchange.)

In the USA, debit cards are usually VISA or Mastercard debit cards, and unlike in Canada, can be used just like a credit card. For any online purchase, you can use your BMO Harris debit card. You may need to provide a 5 digit zip code when you make the purchase, so contact the bank to find out what to enter.

Many businesses rely on personal credit cards for some expenses, which perhaps may have the benefit of accruing points for personal use. If you use your regular Canadian credit card, you may pay a 2.5% foreign transaction fee plus the VISA or Mastercard currency exchange spread (perhaps 0.5%). Alternatives include a no-foreign-transaction fee credit card, a Canadian US Dollar credit card (an annual fee will apply, e.g. TD US Dollar VISA), or a US-based credit card. Cross-border personal banking, from TD Canada Trust or RBC for example, can make it possible to get a personal US credit card based on your Canadian credit rating, and it’s possible to get a credit card without a Social Security Number (SSN). (They’ll probably enter 888-88-8888 or 000-00-0000 for your SSN.)

Regardless of whether you have a Canadian or US credit card, you’ll need a zip code to make a purchase at an American gas pump or ticket machine, or online, and usually this is the trick: Enter the three digits used in your Canadian postal code, plus two zeros.

IRS Form for Customers

On a final note, there’s one more thing that you might not expect as a Canadian. When an American company hires an American contractor, even some incorporated LLC’s, they have to get a W-9 from the contractor and file a 1099 form with the Internal Revenue Service (IRS). Even as a SaaS software vendor, customers have expected this paperwork from my company. There’s no equivalent in Canada; the CRA trusts self-employed Canadians and doesn’t have that additional check to ensure that they report their income. The relevance is that if your company is doing work for a US company or organization, they’re going to expect some paperwork from you, and if they don’t get it, they’re supposed to withhold 30% for the tax man, even though Canada has a tax treaty with the USA to avoid double taxation.

All you have to do is provide your customers with an IRS Form W-8BEN-E. This shouldn’t be too mysterious to them if you tell them it’s just like a W-9. You may or may not need an IRS Employer Identification Number (EIN). The form lasts until the end of the calendar year when it was signed and then the next three years.

I hope this information helps you increase the success and profitability of your export sales, and saves you a lot of time and frustration. Good luck with your venture!

Trevor Cox, BASc MBA

CEO

Appazur Solutions Inc.

© 2021 Trevor Cox